Over the past three decades in the professional liability field, we can observe a recurring underwriting pattern whenever a new operational risk enters the legal marketplace. In the early phase, firms describe the risk in terms of experimentation and efficiency. Carriers initially treat it as a technological development rather than a structural shift. Only later, typically after one or two visible losses, does the conversation mature into questions about supervision, documentation, and institutional controls.

Artificial intelligence is presently in that early phase. Many underwriting applications now contain some variation of the question, “Does your firm use AI tools?” The answers are often brief and reassuring. Some firms respond that AI usage is limited or experimental. Others reference an internal policy prohibiting unsupervised reliance. From a risk perspective, those answers are directionally helpful but analytically incomplete.

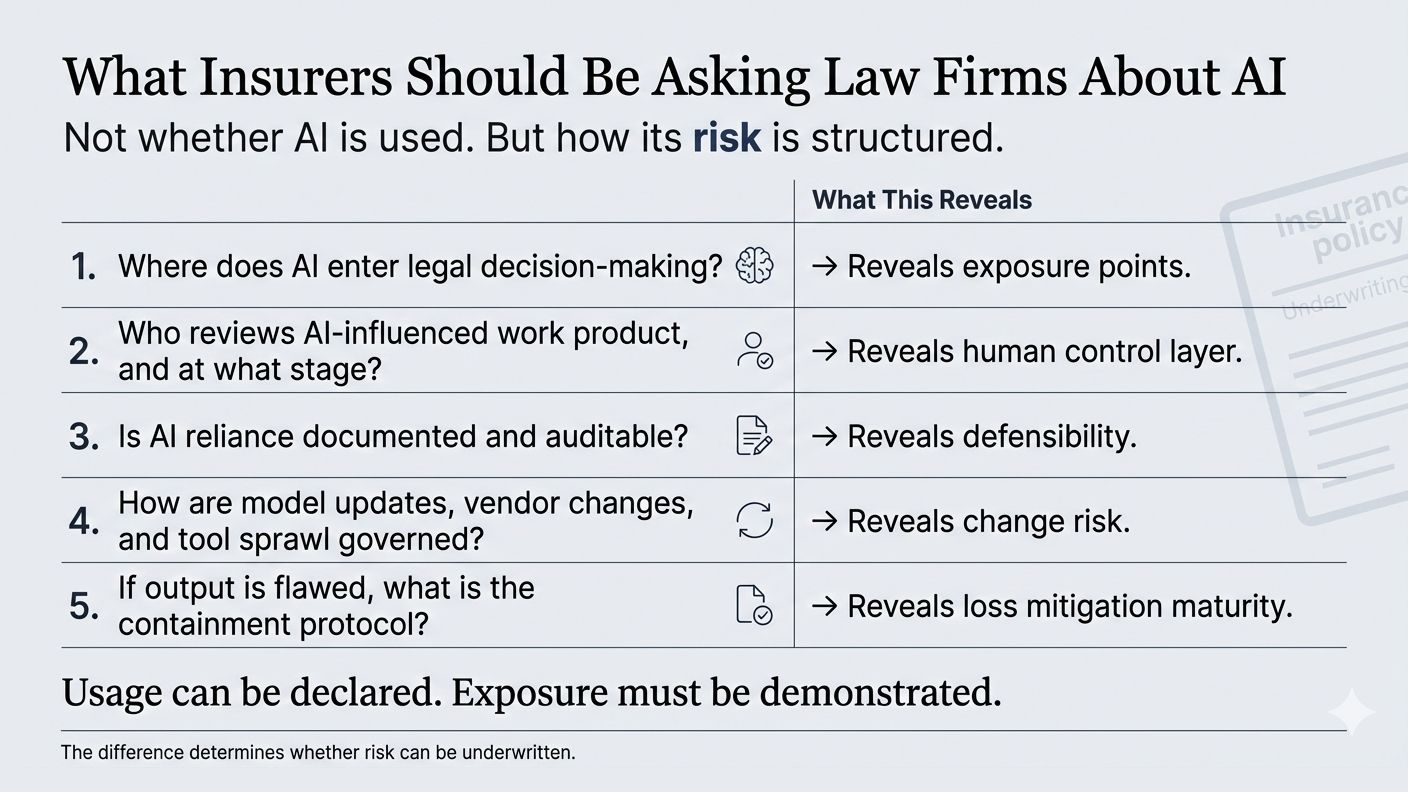

The more meaningful inquiry is not whether AI tools are present. It is how AI integration alters the firm’s supervisory obligations, documentation practices, vendor dependencies, and error propagation dynamics. If carriers wish to assess exposure with discipline rather than optimism, their questions must evolve accordingly.

What follows is not an exhaustive list, but a framework I would expect sophisticated underwriting departments to consider over the next several renewal cycles.

1. Where, Precisely, Does AI Intersect With Client Advice?

Many firms can identify where AI tools are accessible. Fewer can identify where AI output materially influences legal judgment.

An underwriting review should distinguish between peripheral uses, such as internal administrative drafting, and substantive uses that shape research conclusions, transactional language, litigation strategy, or client communications. The distinction matters because liability typically attaches not at the point of tool interaction, but at the point where output becomes integrated into professional advice.

Carriers may consider asking firms to describe:

- Categories of permitted AI use by practice group

- Whether AI-assisted research may be cited directly or how it must be independently verified

- How AI-generated drafting is reviewed before client delivery

- Whether client-facing documents disclose AI assistance when appropriate

A firm that has thought through those distinctions will answer with specificity. A firm that has not will respond in generalities. Underwriting discipline depends on recognizing the difference.

2. What Verification Protocols Exist, and Are They Documented?

AI systems are capable of producing highly persuasive but factually inaccurate output. The risk is not simply hallucination in the colloquial sense; it is the creation of text that appears structurally sound yet embeds subtle analytical error.

The underwriting question, therefore, should focus less on tool access and more on verification architecture. Does the firm require independent source confirmation of AI-assisted legal research? Are supervisory attorneys instructed on how to review AI-drafted material? Is that review process memorialized in policy or training materials?

From a claims-handling standpoint, documentation often determines defensibility. When a client alleges negligent reliance on AI-generated content, the ability to demonstrate a consistent review protocol with an identified escalation path materially affects the evaluation of the matter. Firms that rely on informal expectations of professional judgment may struggle to produce evidence of systematic oversight.

Carriers are accustomed to evaluating cybersecurity controls, conflicts checks, and docketing systems. AI verification protocols should be viewed through a similar lens.

3. How Is Vendor Risk Being Assessed?

One of the more underappreciated dimensions of AI exposure arises through third-party integration. Established legal research platforms, document management systems, and practice management software increasingly incorporate AI features by default. Firms may not perceive these integrations as affirmative AI adoption, yet client data may nonetheless be processed through external models.

Underwriters may reasonably inquire about:

- Contractual representations regarding data retention and model training

- Indemnification provisions tied to AI-related failures

- Limitations of liability embedded in vendor agreements

- Internal review procedures for new technology deployments

Historically, malpractice exposure has often intersected with vendor relationships in the context of e-discovery and cybersecurity incidents. AI introduces similar vectors, with the added complexity that data may be used to train models beyond the firm’s immediate control if contractual protections are inadequate.

The underwriting file should reflect not only that the firm has vendor agreements, but that someone with appropriate authority reviews AI-related clauses with an understanding of professional confidentiality obligations.

4. Who Within the Firm Has Formal Oversight Responsibility?

In emerging risk categories, responsibility frequently fragments. Innovation committees explore capability. IT departments manage deployment. Risk management addresses insurance implications. Executive committees assume someone else is synthesizing the information.

From a liability perspective, diffusion of responsibility creates vulnerability. When no single role carries defined oversight authority, governance becomes aspirational rather than operational.

Underwriters may consider asking firms to identify:

- The individual or committee formally charged with AI governance

- Reporting lines to executive leadership

- Frequency of review and update of AI-related policies

- Mechanisms for incident reporting and escalation

This line of inquiry is not adversarial. It is clarifying. Firms that have centralized oversight tend to respond coherently. Firms that have not often rely on broad assurances about professionalism. Professionalism is essential, but it does not substitute for structure.

5. How Is Training Being Delivered and Measured?

Training represents one of the most tangible underwriting signals. A written policy without education often reflects symbolic compliance. Training that addresses practical scenarios, by contrast, suggests operational seriousness.

Carriers might explore:

- Whether AI training is mandatory or optional

- Whether it is tailored by practice area

- How frequently it is updated

- Whether attendance and comprehension are tracked

In malpractice litigation, training records frequently surface in discovery. They become part of the narrative regarding foreseeability and reasonable care. Firms that can demonstrate structured instruction on AI risks will be positioned differently than those relying on informal guidance.

6. How Does the Firm Monitor Emerging Developments?

AI capabilities are evolving rapidly. Governance that remains static for several years will likely become outdated. Underwriters may therefore evaluate whether firms conduct periodic reassessments of AI policies and practices, particularly as tools change and regulatory guidance develops.

This does not require constant reinvention. It does require scheduled review, documented discussion at the executive level, and willingness to revise protocols as experience accumulates.

From a portfolio perspective, carriers should also consider aggregation risk. If multiple insured firms rely on similar tools with similar verification weaknesses, a single widely publicized failure could influence claim frequency across the book. Understanding how each firm monitors developments provides insight into correlated exposure.

A Forward-Looking Underwriting Posture

The objective of these inquiries is not to discourage innovation. It is to distinguish between firms that integrate AI within a disciplined supervisory framework and those that assume traditional professional judgment will adapt automatically.

In prior cycles involving electronic discovery and cybersecurity, early underwriting questions were narrow. Over time, they expanded to include written policies, designated officers, training documentation, and vendor controls. AI will likely follow a similar trajectory, though perhaps on an accelerated timeline.

Insurers who refine their questions now may gain two advantages. First, they can differentiate risk quality within their portfolios before claims data becomes statistically meaningful. Second, they can encourage insured firms to adopt governance measures that reduce the likelihood of future loss.

For law firms, these underwriting inquiries should not be viewed as intrusive. They are signals. Carriers are indicating that AI has moved from novelty to exposure category. Firms that respond with specificity and documentation are not merely satisfying renewal requirements; they are strengthening their defensibility in the event of scrutiny.

The central issue is not whether AI tools are used responsibly in isolated instances. The issue is whether the firm can demonstrate, if asked under oath, that it approached AI integration with the same deliberation applied to conflicts management, docket control, and client confidentiality.

Underwriting applications will continue to evolve. The more sophisticated the questions become, the clearer it will be that AI is no longer being evaluated as a technology add-on but as a component of enterprise risk. Carriers and firms alike would be well served to anticipate that shift rather than react to it.

Questions to Consider

- Could our firm clearly explain where AI influences legal judgment?

- Are our verification requirements documented and consistently applied?

- Who would be responsible for explaining our AI governance program during a malpractice claim?

- Have we evaluated AI-related vendor risks with the same rigor applied to cybersecurity vendors?

- Would our underwriting application accurately reflect our actual AI usage and governance practices?

Next Steps for Law Firms

- Assess current AI usage across practice groups and identify where AI influences legal advice.

- Document AI verification procedures for research, drafting, and client-facing communications.

- Review vendor agreements for AI-related confidentiality, liability, and data usage provisions.

- Assign formal AI governance responsibility to a designated individual or committee.

- Implement role-specific AI training and maintain evidence of participation.

- Conduct periodic reviews of AI policies as technologies and regulations evolve.

Next Steps for Insurers and Underwriters

- Expand underwriting questionnaires beyond simple AI usage disclosures.

- Develop evaluation criteria for AI governance maturity, verification controls, and oversight structures.

- Review policy language for AI-related exclusions, limitations, and coverage ambiguities.

- Assess aggregation risk arising from common AI vendors, platforms, and workflow dependencies.

- Incorporate governance indicators into underwriting and renewal assessments.

- Consider premium incentives or preferred underwriting treatment for firms demonstrating mature AI governance practices.

- Establish underwriting guidance for evaluating AI-related vendor risk and contractual protections.

- Monitor emerging claims, regulatory developments, and industry loss trends to refine underwriting standards.

Related Topics for This Article

- AI Governance for Law Firms

- Professional Liability Insurance

- AI Verification and Validation Controls

- Legal Malpractice Risk Management

- Underwriting Emerging Technology Risks

- Vendor Risk Management

- AI Policy Development

- Enterprise Risk Governance

- Legal Ethics and Artificial Intelligence

- Documentation and Defensibility

- Risk-Based AI Oversight

- AI Governance Maturity Models

Related Articles

- AI Adoption Is Outpacing AI Governance in Law Firms

- The Difference Between AI Usage and AI Exposure: What Law Firms and Insurers Need to Understand

- When AI Uncertainty Arises, Who Decides? Designing an AI Governance Structure for Law Firms

- Future: How to Audit AI Usage Across Practice Groups

- Future: The Hidden Vendor Risks Embedded in Legal AI Platforms

- AI Creates Professional Liability Risk, Not Just Technology Risk

- Future: From AI Policy to AI Governance: Understanding the Difference

- AI Governance Is Not an IT Problem: Why Leadership Must Own the Risk

- Culture Follows Leadership: The Hidden Role of AI Governance